移民澳洲后,在澳洲工作的你退休后可以享受澳洲的养老金(Super)。

而且,如果您之前在中国工作过,有在中国积攒的社会保险,你可以将已缴纳的部分保留下来,继续缴纳满15年。

这样的好处在于,您在退休后,即使身在国外,也能够与国内的老人一样领取中国的退休金!加上您在澳洲的养老金,您退休后将可以领取双份的养老金!

下面我们会对此做一个具体的讲解。

中国社保

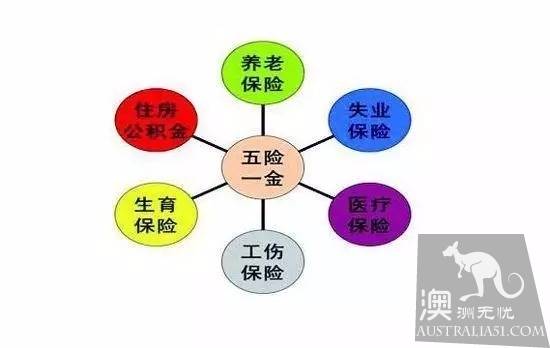

区分“社会保险“与“五险一金”

社会保险包括养老保险、医疗保险、失业保险。很多人可能对“五险一金”(养老保险、医疗保险、失业保险、工伤保险、生育保险&住房公积金)和社会保险的概念有混淆。

大家不妨这样看,“五险一金”中的“三险”,即老保险、医疗保险、失业保险,是最基本的社会保险,即我们常说的“社保”。缴纳三险是国家社保政策规定的,只要你与所在单位签署了正是劳动合同,单位就应该为你投保。

对于中国的社保部分,简单来说,你有两种选择:退保或者不退保。

看似简单,但其实需要大家在了解相关政策的基础上,结合个体情况与需求,做出自己的选择。一旦选择退保,操作不可逆,也就是说,如果想再加入,保险需要清零重新缴纳和计算。

推荐方案:不退保,继续缴纳至满15年后,到退休年龄正常领取退休金。

按照目前的政策,男性职工在年满60岁,女性职工满50岁,社保缴费满15年后就可以办理退休领取退休金。

但注意如果出国中途中断的话,必须重新缴费满15年才可以领取。

即使您在国外居住,社保经办机构可以将其每月的退休金寄给参保人。每年一次的领取养老金资格认证,也可以在当地的中国大使馆进行认证之后寄送回国。

所以,如果不是急需用钱,出国后仍然继续缴纳社保,到了退休年龄后正常领取社保是一个非常稳健的选择。

待选方案: 我一定要退保

如果您一定想要退保,拿回已缴纳的部分,停止缴纳以后的保险金额,也是可以的。移民后,理论上讲养老保险、医疗保险和住房公积金是可以部分支取的。不过每个地方细则上可能会略有差异。

根据中国相关政策规定,参保人退休前出境定居,个人账户储存额退还给被保险人,同时终结养老保险关系。

您需要做的,就是带上您的

-

社保卡、公积金卡

-

澳洲护照原件和复印件(如果已经入籍)

-

注销户口证明的原件和复印件

-

身份证复印件或中国护照复印件

到相关机构注销社保账户和公积金账户,取出余额就可以。

当然,如果选择退保,你退休后就无法再领取中国的退休金了。

总的来说,移民澳洲并不影响中国退休金的领取,因此,大多数人会选择不退保。而且,退保时,只有公积金是可以全部退还给个人的,养老金只能退个人交的部分(因为养老保险、医疗保险和失业保险是由企业和个人共同缴纳的)。

澳洲养老金(super)

了解澳洲养老金,调整储蓄习惯进行合理的投资,将会为退休后的生活带来更充裕的资金,让您无忧无虑坐看夕阳。

这里先简述一下澳洲养老金的重要基本概念:

澳大利亚养老金superannuation是一种退休保障体系,简称super。

法律强制规定雇主为员工缴纳工资一定比例的金额,也可以个人自愿供款到专门的养老金基金管理公司或自行管理养老金基金(SMSF)。个人达到规定的退休年龄或满足其它条件(比如伤残、财务危机、离境定居)时,可以一次性或分期取出养老金账户里的钱,也可以以年金形式取得长期收入。通俗地说,这就是给退休后的你留的钱。

澳洲现行法律要求企业必须缴纳的Super 是基本工资的9.5%(前些年的要求还是9.25%)。大多数可能还不知道,政府规定的养老金比例还会继续上调,按照目前的计划, 2021年养老金比例将增长到10%,而2025年之后更增至12%!

还有一些您有必要了解的常识:

1. 雇主必须按照不低于工资9.5%的标准为雇员缴纳养老金。

2. 你的养老金必须至少每三个月存入一次。如果雇主没有按时缴纳,你可以向澳洲税务局举报。

3. 月收入高于$450的雇员才有权利获得养老金。18岁以下的人员必须月收入高于$450并且工作时长超过30个小时以上。

4. 近些年更新的规定:70岁以上的工作人员也是有权获得养老金的。2013-2014财年之前,按照旧规,雇主是可以不用支付的。

5. 自雇人群也有权利获得养老金。如果您的个人收入主要是来源自己运营的生意,您就有权利给自己交可抵税的养老金(deductible superannuation contribution)。

注意,Super不同于Age Pension。后者是政府根据退休人员的收入和资产情况提供的福利。Super的余额和来自Super的收入越多,可领取的Age Pension越少,再考虑到其它收入和资产,按照一定的计算公式减至零为止。所以Super就是政府为了满足未来社会保障的一种强制手段。一般来说,Super里面还可以包含一系列的保险,有兴趣的话大家可以自己再去详细了解。

在这样的澳洲现行养老体系下,移民澳洲的人其实在年老时本身就拥有了较为丰厚的养老收入。

再加上在中国积攒的社会保险,让您退休后在中国还有一部分收入。那么,相信您的退休生活一定是这样的: