澳大利亚税务系统是一个非常复杂的概念,但与每个人,每个家庭都息息相关。澳洲的税收系统极其完备,与中国税务系统也存在者很多差异性。那么,它是怎么运作的呢?今天我们就给大家简要介绍一下澳洲的税收系统。

首先,我们先来了解一些税收方面的基本概念

税务居民 (Australian resident for tax purposes) 与非税务居民 (foreign resident for tax purposes)

税务居民跟永久居民(PR)是不一样的概念。税务居民跟非税务居民界定取决于很多因素,一般来说看停留在澳洲的时间,如果在澳洲停留半年以上,为税务居民,否则为非税务居民。举个例子,到澳洲学习的留学生持有的是学生签证,但由于停留时间在半年以上,留学生属于税务居民。又例如澳洲PR常年停留在中国,只是偶尔到澳洲度假游玩,在澳洲停留时间在半年以下,这类持有澳洲PR也属于非税务居民。

作为税务居民,在澳洲应纳税收为:最终应纳税(Tax Payable)=所得税(Tax on income)+医疗保险税(Medicare Levy)-税收抵免(Tax offset)-已缴税款(Tax Credit)

所得税 (Tax on income)

所得税取决于应纳税额(Taxable income)与边际税率(Marginal tax rate)。应纳税额等于应纳税收入(Assessable income)- 允许扣除额(allowable deduction)。

边际税率 (Marginal tax rate)

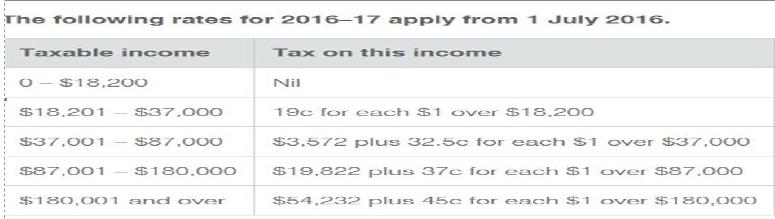

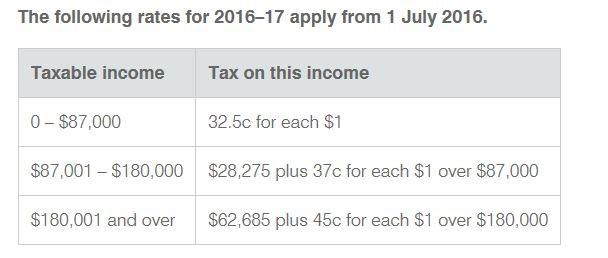

如图一和图二分别是2016/2017税务居民和非税务居民税率表:

图一:2016/2017税务居民税率表(来源:ATO)

图二:2016/2017非税务居民税率表(来源:ATO)

医疗保险税 (Medicare Levy)

一般为应纳税额(Taxable Income)的2%,但对于低收入者有减免。不享有澳洲本地医疗福利(Medicare Benefits)的居民 (例如非PR)无需缴纳医疗保险税。

税收抵免 (Tax offset)

最常见的为低收入税收抵免(Low income tax offset)和红利抵免(Franking credit)。

低收入税收抵免指的是居民收入低于66,667澳元可获得最多445澳元的税收抵免。以下表格反映了低收入税收抵免情况(2016/2017):

应缴税收收入(Taxable income) 税收抵免(Tax offset payable)

≤$37,000 $445

$37,001-$66,666 $445-[(Taxable income-$37,000)*1.5%]

≥66,667+ NIL

来源:澳大利亚税务局(ATO)

红利抵免(Franking credit)

是指当投资者取得一家企业的分红时,可能会随附“扣缴税额”,因为该企业已经为此支付了利润税。扣缴税额可以大幅降低投资者所获红利要支付的税款。