前言

澳大利亚地产业规模高达7万亿,而7万亿的市场足以牵动澳大利亚的整体经济。鉴于体量庞大,房价又跌跌不休,很多人开始质疑眼下的澳洲房市到底是“正常的周期性调整”,还是属于“泡沫吹大后的梦魇”?

一 第二个爱尔兰?

澳大利亚数据金融分析公司(Digital Finance Analytics)负责人Martin North表示,未来12-18个月,澳大利亚或将成为第二个爱尔兰。

回溯至金融危机爆发期间,爱尔兰因为房地产泡沫而深陷危机的情景历历在目,银行被无法回收的房贷拖垮;一些新建成的小镇因无人买房居住变成“鬼城”;许多来自东欧和亚洲的员工因为工资、福利下降纷纷出走他国。迫于无奈,爱尔兰不得不向欧盟和国际货币基金组织发出援助请求。

全球专业基金巨头富达(Fidelity)澳大利亚董事总经理Devoy来自爱尔兰,她曾亲历了爱尔兰住房市场破灭的全过程。

在近期庆祝公司新兴市场基金成立的一次活动上,Devoy表示,澳大利亚财富过度集中在了住房市场,无论是通过直接住房投资,还是通过大银行退休基金进行投资等方式。她说:“包括负债收入比、房价收入比、房价收入比等在内的所有指标均表明澳大利亚住房市场一个巨大的泡沫正在形成。”

但是,Devoy认为尽管澳大利亚住房市场存在泡沫,但是和爱尔兰当时的情况存在明显差异。例如,爱尔兰央行实行的是德国、法国等欧洲国家的货币政策。当时,爱尔兰人贷款成本接近0,导致几乎每个人都是开发商和借款人。实际施工率是需求量的两倍。但是澳大利亚目前的情况并非如此。

澳大利亚数据金融分析公司(Digital Finance Analytics)负责人Martin North则表示,尽管澳大利亚和爱尔兰存在一定的差异,但是在很大程度上是完全相似的。

他说:“如果把爱尔兰住房市场泡沫破碎前1-2年内出现的各种不同因素和目前的澳大利亚住房市场进行比较,你会发现两大市场相似之处远远大于差异。”

首先,爱尔兰实施的是非常宽松的货币政策和贷款政策。同样,澳大利亚央行已经连续25个月维持1.5%的低利率不变。尽管贷款政策有所收紧,但是仍然处于相对宽松的状态。

其次,爱尔兰建筑业经历了一个显著的增长时期。当时,首次置业者直接选择门槛较低的新建公寓,随后公寓新建热潮导致供过于求,继而引发崩盘。同样,在澳大利亚我们也看到目前的新建公寓量也面临非常重大的风险。我们看到很多新建的公寓出现销不动的情况,很多开发商也面临资金链断裂的风险。

来自爱尔兰的悉尼大学经济学教授Colm Harmon对目前澳大利亚住房市场的风险也持相似的观点,即目前的澳大利亚住房市场和爱尔兰市场非常相似。

目前,澳大利亚住房市场最大的风险即皇家委员会所暴露出来的问题,即低廉的贷款成本和宽松的贷款条件。

他说:“尽管利率有所收紧,但是贷款买房人能否承受则成为了关键。尤其是当大量只付息贷款到期转换为本息同还贷款的情况下,贷款买房人能否承受。”

大量新建的房屋或许能显示一个国家的经济繁荣,但其背后的隐患是巨大的泡沫。有数据表明,从1996年到2006年,爱尔兰房价平均上涨了三四倍,房价相对家庭年收入的比值也从4增长到10,在都柏林,房价与收入比高达17。

二 澳大利亚第三季度房价

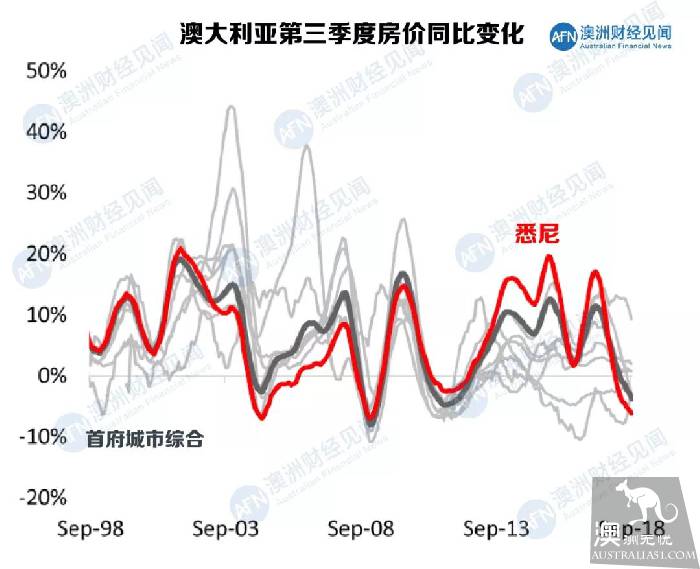

今年第三季度,澳大利亚房价环比跌幅有所扩大。其中,悉尼录得全澳最大同比跌幅,下跌6.1%。

今年第三季度,悉尼房价环比下跌1.5%,同比则下跌6.1%。其中,独栋屋和公寓同比分别下跌7.6%和2.6%。

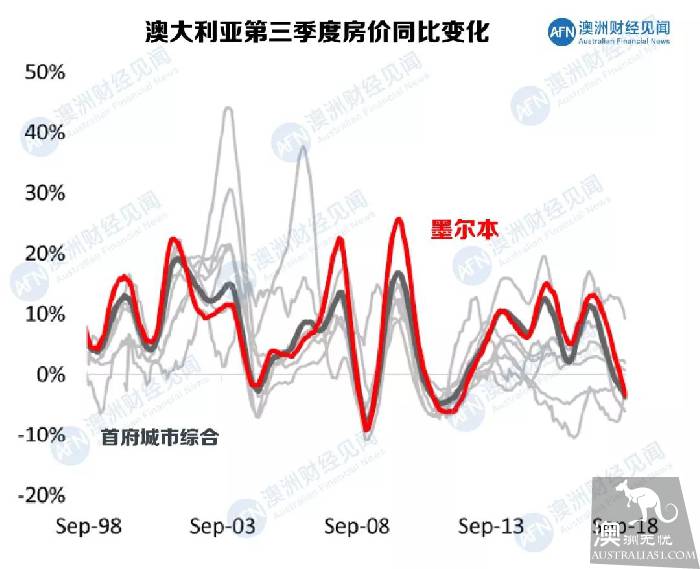

墨尔

今年第三季度,墨尔本房价环比下跌2.4%,同比则下跌3.4%,较2017年11月峰值跌幅达到4.4%。

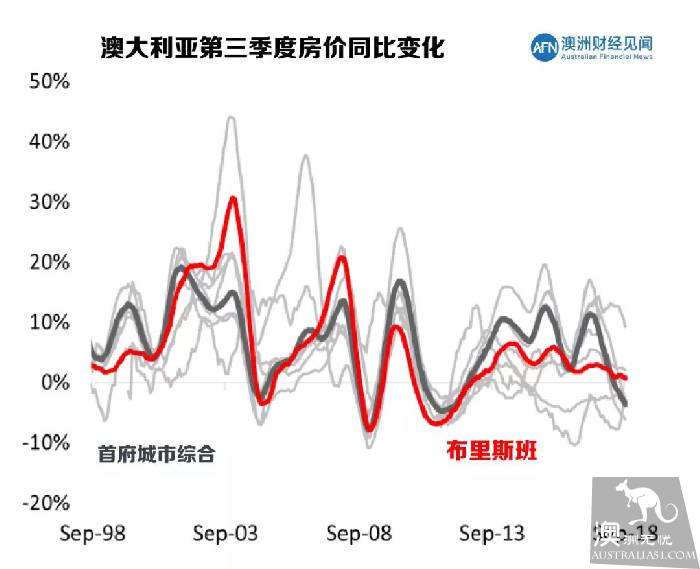

今年第三季度,布里斯班房价环比上涨0.1%,同比则上涨0.8%。其中,独栋屋和公寓同比分别上涨0.8%和0.7%。

今年第三季度,阿德莱德房价环比持平,同比则上涨0.7%。其中,独栋屋和公寓同比分别上涨0.6%和1.2%。

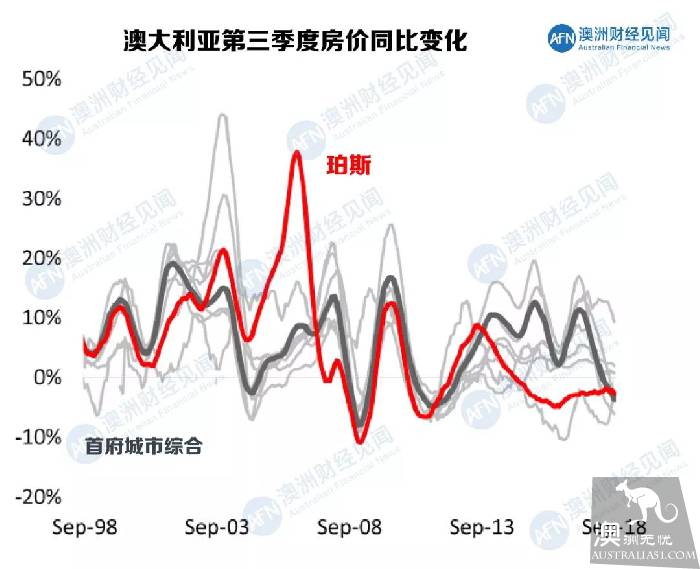

今年第三季度,珀斯房价环比下跌2.0%,同比则下跌2.8%,较2014年6月高点已经下跌13.2%。

三 利好VS 利空

如前文所讲到的,目前关注的焦点是澳大利亚住房市场的泡沫是会逐步萎缩,还是会直接破灭?换言之,目前澳大利亚住房市场所面临的利好和利空有哪些?

利好

事实上,在本轮暴涨之前,澳大利亚住房市场曾经经历了长时间的下跌,即19世纪90年代早期和20世纪30年代,最严重的两次下跌都和全球经济衰退有关。同时,复苏过程漫长而痛苦。

除此以外,绝大部分时间,澳大利亚住房市场都是经历正常的周期调整,下跌幅度大约在10%,随后会出现明显的回升。

因此,支撑市场相信本次不是泡沫崩盘而是正常调整的“利好”条件包括:

以美国为代表,全球经济正在走强;

澳大利亚就业持续保持强劲;

澳大利亚经济增长稳定,今年第二季度同比增长3.4%;

澳元兑美元汇率跌至0.7000,有助于确保本地经济;

澳储行在未来一年内进行加息操作的几率并不大。

但是,支持市场调整,房价进一步下行的利空因素也同样存在。

信贷收紧导致房价下跌。借款人可用现金减少意味着对住房的需求减少,进而影响房价下跌。

融资成本上升。目前,过去几年,美联储先后已经八次加息。由于澳大利亚主要大银行均依靠海外融资,因此,融资成本上升是大势所趋。

另外,房地产市场面临的最大威胁是失业。尽管截至目前,就业增长势头良好,但是如果东海岸房地产价格下跌导致住房建设热潮停滞不前,会发生什么?

毫无疑问,失业率将大幅上升。 这意味着房屋贷款违约增加以及强制销售后房地产面临进一步压力。在这种情况下,全国房价肯定会远低于大多数人所预期的10%的跌幅,继而导致很多在过去两年内买房的人资不抵债。

四 何时才能入场?

在住房市场疲软,负面报道铺天盖地的情况下,在买房问题上,人们可能会三思而后行。

澳大利亚权威房产机构CoreLogic提供的数据显示,截至今年9月,全澳范围内房价同比已经下跌2.7%,拍卖清空率降至60%以下。

在悲观情绪影响下,一些投资者会认为,由于近年来房地产行业累积涨幅过大,未来几年不可避免地表现不佳。他们大都预测房价会下跌10%,15%或20%。

的确,很多人认为,即使目前房价出现下跌,但是价格仍然超出了自己的可负担范围。市场一旦过头就需要进行纠正,目前的市场表现亦是如此。尤其是在信贷收紧、皇家委员会调查的影响下,很多潜在买房人都进一步下调了购房预算的标准。

但是,也有市场人士指出,并不是所有的上涨背后都伴随着下跌。同时大批人士均认为目前的澳大利亚住房市场并没有达到泡沫的状态。

原因很简单,在他们看来,人口持续增长、国民经济强劲、利率持续低位等基本面支撑因素并未发生改变。

此外,澳大利亚的住房需求仍然很大,同时我们还没有足够的新建住房来满足这种需求。只要供需不匹配持续,房地产价格的下行风险就会相对要低

但是,这样是不是就意味着我们应该入市呢?

从投资的角度而言,住房投资关键的应该是取决于投资者的个人能力,而不是倾尽所有博一回市场。

如果投资者了解房产投资是一项长期的投资,并且选择了正确的投资资产,则可以顺利避免任何市场波动。

现在是入市的好时机吗?如果想要在1-2年内获得较大的资本利得,那么现在显然不是好的时机。但是,从长远来看,优质物业具有良好的投资回报。原因很简单,优质资产需求大且相对稀缺。尤其是在市场条件不好的情况下入手也符合市场的规则。

END

任何投资都有风险,风险越大,投资回报越高。住房投资亦是如此,只要买进就挣钱的日子已经过去,在市场波动时期考验的更多的是投资者的耐心和选择。