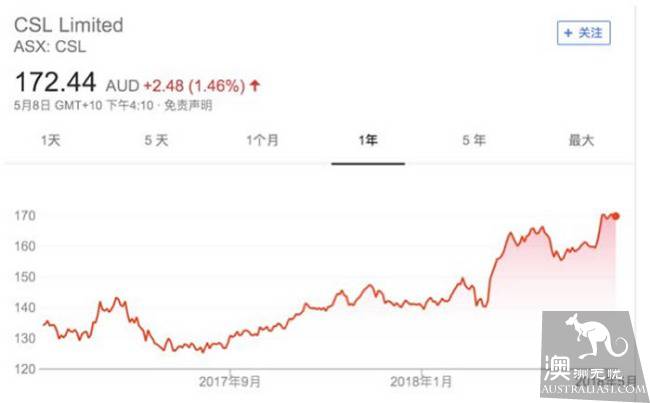

现在说起CSL,很多投资者的第一印象都是昂贵的股价。的确,目前公司172.72澳元的交易价格在整个ASX200中也可以说是名列前矛。目前外界普遍对其的描述都是“血液制造巨头”,事实上这一称呼略微有点以偏概全的意思。

CSL Limited是全球专业生物技术公司,研究,开发,制造和销售产品治疗和预防严重的人类疾病。产品范围包括血浆衍生物,疫苗,血清,用于各种医学和遗传研究和生产应用的细胞培养试剂。

公司的前身是成立于1916年的联邦血清实验室,当时是专注于疫苗制造的澳大利亚政府机构。目前公司主要业务之一的血浆分离业务开始于1952年,当时距离实验室成立已经过去了将近40年的时间。

1994年的时候,这个政府实验室正式私有化成为CSL公司,并在ASX挂牌上市,当时的发行价是每股2.30澳元。2000年通过购买一家瑞士血浆公司,位于伯尔尼的ZLB生物血浆公司,公司规模增加了一倍,股价也一路高歌猛进。

很多投资者对于这种高股价的个股都存在一定的顾虑,一方面是投资金额,另一方面就是担心其股价太高,后劲不足。那么这一情况在CSL中是否也同样存在呢?

具体分析

从晨星(Morningstar)最新的研报上来看,CSL在寡头垄断行业内不断成功的创新支撑了其业务增长和盈利能力,并且公司在近几年来不断开拓新兴市场的份额。分析师认为CSL在血浆分离业务上依旧具备长期的盈利前景。

分析师对于CSL的公允价值(FV)估值为每股145澳元,并预计截至2020年6月的,公司的复合年增长率为12%,营业利润率为18%,税后净利润增长19%。 主要驱动因素是新兴市场的需求增加以及产品创新持续成功。

而对于公司的风险,相比财务数据,分析师认为产品本身的意外性或许更有可能成为股价下行的原因。由于血浆产品用于重症患者,所以一旦有害的副作用或产品质量问题出现,将会成为公司巨大的风险。

比如在1928年的时候,公司生产的一批白喉抗毒素牵涉到12名儿童死亡,在后来被称为“班达伯格悲剧”,这一事件在当时可以说是摧毁了公司的公信力。除此之外,作为一家生物科技公司,CSL还面临着物质专利或知识产权纠纷可能导致重大业务中断的一般行业风险。

单从财务数据来看,CSL可以说是无可挑剔,虽然短期内公司在新兴市场的利润率较低,但在适度的经营杠杆下,这将在未来几年内实现两位数的利润增长。综合来看,晨星(Morningstar)认为CSL适合那些了解生物科技领域固有风险的成长型投资者。